Our data on health premiums has been pretty bad. Not anymore.

By Sarah Kliff, July 24, 2013 - Washington Post

Get excited health-care world: I think I’ve found my new

favorite Government Accountability Office report, perhaps the most

scintillating of their works since “Status

of CMS Efforts to Establish Federally Facilitated Health Insurance

Exchanges,” which was, admittedly, also a page-turner.

The report came at the request of Sen. Orrin Hatch, a Republican who

represents Utah. He wanted to know how much health insurance costs right this

moment, which could help us better understand how the marketplace will change

with the Affordable Care Act.

On Monday, the Government Accountability Office sent back a thick stack of

insurance data, broken down by state, explaining the cost of health insurance.

Analysts there used data from HealthCare.Gov, a new site created under the

Affordable Care Act where insurers post their offerings and how much they

cost.

The database, the GAO analysts admit, isn’t perfect. About 20 percent of

insurers don’t post their plan data, which means we’re missing about one-fifth

of the marketplace. There’s no enrollment data, which means some of the options

listed may not have any subscribers.

Still, this is probably the best data set we have on insurance premiums so

far. It’s also a dense report, 62 pages of line-by-line data that I’ve found a

bit easier to digest in a chart.

What you see below are premiums from 10 states and the District of Columbia

for a 30-year-old female who does not smoke and has not yet been underwritten

(read: She could face a higher charge, if she has a preexisting condition).

I chose these states because these are the ones

that Health and Human Services used in its report last week, which looked at

premiums under the Affordable Care Act. As for the demographic element, the GAO

only broke out data for certain types of insurance subscribers. I picked out

one, but you can see the rest in the full report.

Without further ado, here’s what premiums look like right now for a young

woman purchasing her own health insurance coverage:

A few things stood out to me here.

Some young, healthy adults can buy really cheap insurance right

now. In most states, a 30-year-old without preexisting conditions

can purchase a health insurance plan for about $55. New York’s premiums are a

notable exception to this for reasons explained here. Washington and Rhode

Island I’m less familiar with and not quite sure why their premiums are so much

higher than the rest.

But not all of them: One in five applicants on HealthCare.Gov are

rejected. The data you see before is all before underwriting, where

insurers figure out the amount they should actually charge a

subscriber –– or if they even want to insure that person in the first place. A

separate GAO

study found that 19 percent of applicants for coverage on HealthCare.Gov are

rejected by the insurance company. With some plans, the number is as high as 70

percent.

That coverage will be really

skimpy. The majority of those plans in the $50-range have a

deductible of $10,000. Vermont’s $55 offering has an impressively

large $100,000 deductible (no, that last zero is not a typo).

This is something that will be very different under the Affordable Care Act,

where cost sharing for an individual (not just the deductible, but all the

co-pays too) is limited to about $6,000. There’s a debate over whether this is a

good thing; some argue that this forces young adults to buy coverage more robust

than what they need. But what both sides do agree on is that plans sold on the

new marketplaces will be more robust than what’s on the market right now.

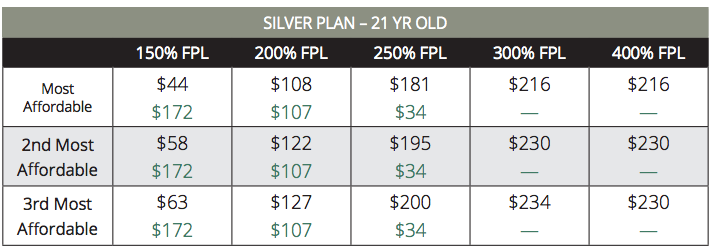

Some young adults will still get insurance for $55 under Obamacare.

Some won’t. It all depends on their income level, which determines

the level of subsidies that an individual receives. California, for example,

estimates that a young adult at 150 percent of the federal poverty line would be

able to purchase a health plan for $44 per month:

A 21-year-old who received no subsidy at all, by contrast, would face a $172

premium for the same insurance plan.

It’s still hard to compare premiums pre- Obamacare and

afterward. You’ll notice that the numbers in my chart are significantly

lower than those in HHS’s

estimates of average premiums under Obamacare. I would caution against

reading too much into that.

Part of the difference is undoubtedly due to the Affordable Care Act:

Premiums increase when sick people enter the market, and policies are required

to cover more benefits. But another part of it is a less sexy issue of data

formatting that makes the HHS and GAO data a bit of an apples-to-oranges

situation. The HHS data are capturing both Obamacare policies and the cost of

insuring older adults, and any comparisons to the GAO figures should probably be

made with a massive grain of salt.

KLIFF NOTES: Top health policy reads from

around the Web.

Hospitals are gearing up for a big Obamacare push. “Big

chains, publicly owned safety-net facilities and local hospitals are ramping up

their efforts to be ready for the six-month open enrollment period for 2014

health insurance that begins Oct. 1, when the health insurance exchanges for

people who don’t get health benefits at work are due to open for business. How

well they do could go a long way to determining the success of Obamacare’s first

year.” Jeff

Young in the Huffington Post.

Congratulations Wisconsin and Virignia, you’re the lowest Obamacare

spenders! “Only one state will spend less per capita than Virginia

to promote public awareness of the new health care reform law. According to

data compiled by The Associated Press from federal and state sources, the $3.9

million in outreach spending in Virginia amounts to 49 cents per resident. Only

Wisconsin, at 46 cents, is spending less per capita.” The

Associated Press.

Of course Oregon’s fight over Obamacare is being fought with…acoustic

guitars. “Ben Nanke, a 20-year-old aspiring songwriter and

filmmaker from Salem, admires the musicality of the ”Cover Oregon” ads

promoting the state’s new health care exchange. But Nanke, a registered

Republican and self-described libertarian, doesn’t think much of Obamacare, or

any government-run health care for that matter. So with some friends, he created

his own music video championing the virtues of rugged individualism.”